Hack Together a Debt Snowball Calculator With Python

The Debt Snowball is a repayment strategy that prioritizes paying back loans with the smallest balances first. This method is widely touted as being successful not for its mathematical superiority but buy its ability to take advantage of human psychology. The Debt Snowball Calculator can help identify the exact payment requirements… and outcome.

The Debt Snowball is a repayment strategy that prioritizes paying back loans with the smallest balances first. This method is widely touted as being successful not for its mathematical superiority but buy its ability to take advantage of human psychology. The Debt Snowball Calculator can help identify the exact payment requirements… and outcome.

Dave Ramsey, the personal finance guru himself, advocates for the use of the Snowball Method (as opposed to the Debt Avalanche). But how does someone plan various scenarios with this payment strategy given the complexity and tediousness of the math involved?

With a few lines of Python code, you can quickly and seamlessly automate a repayment schedule built around the Snowball Method.

In this article I will show how to code your own Debt Snowball Calculator in Python. I will cover how to create your own snowball function and plot out relevant results using the Seaborn library to analyze whatever financial scenario you throw at it.

Importing the Required Loan Information for a Debt Snowball

In order to compute the Debt Snowball payment schedule, we need to know the details of all of the loans. The 4 components of each loan that needs to be imported are:

- The Name of the Creditor

- The Current Balance of the Loan

- The Interest Rate of the Loan

- The Current Minimum Payment of the Loan

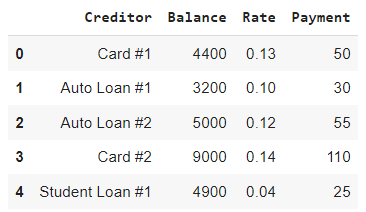

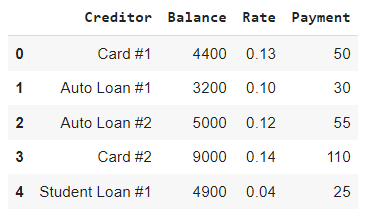

I have chosen to use a simple Excel file as a way to input this information for import into a pandas environment.

The format I used was a replica of the input cells required for our benchmark, the spreadsheet available from Vertex42 and can be seen below. You can very easily recreate this quickly for your own purposes.

The code below uses Pandas to import this spreadsheet directly from a local directory. If you are using Colab, simply drag and drop the excel file onto the file folder on the left side navigation pane.

Sorting the Loans by Balance

Since the Debt Snowball needs the loans to be sorted by balance we will go ahead and do that below. If we chose to instead sort by highest interest rate, then we would inadvertently be using the Avalanche Method.

As can be seen above, if we add all the minimum payments together you get $270. Since the max we can pay each month is $500 the snowball will be $230. As we begin to pay off loans entirely, the snowball will start to grow and our ability to tackle the larger debts will increase.

Tracking Payoff Month

Now we need to add an additional column to keep track which month is which. The initial data will be denoted as Month ‘0’ and the value will increase until the loan is paid off completely.

Preparing Tracking Variables for Our For Loop

Next, I will setup a for loop to test that our calculations come up with the right answer. It is always best to verify the methodology before you implement it after all.

Initializing the variables necessary for the loop comes first. numOfLoans is simply the number of creditors. This list is what will be looped through.

The variable workingSnowball is the amount of the snowball available to pay the next loan. This will include additional snowball if a loan gets paid off at some point or less snowball if a previously loan used some or all of it.

loanInformationMonth1, a DataFrame, will be used to store all the results for this test run of our calculations.

Below is the output of the for loop found in the DataFrame loanInformationMonth1 .

As we can see above Card #1 was paid down in the following manner:

The Principal Payment + The Snowball = $2.67 + $230.00 = $232.67

Thus, since the starting balance was $3,200, the new balance should be approximately $2966.32. This is nearly exactly what we were able to calculate using the code above.

But how do we apply this same methodology month in and month out?

Modifying the For Loop to Calculate all Payoff Data

Next, we need to figure out a way to iterate through each month while keeping tabs on our occassionally changing snowball.

My solution proposes that it would be beneficial to save all data collected along the way. To do this we will use a an expanded version of the same DataFrame to store additional results. This includes the partial interest and principal components for each payment and the total monthly amount applied for each loan.

We will need to approach the snowball method much in the same way as above except we will need move down the DataFrame for each month as we iterate through. We will keep a record of all transactions.

There will also need to be a while statement to determine if and when all balances have reached 0. This will prevent us getting caught into an infinite loop. Eventually we will move towards turning this into a function so this whole complicated looping business is invisible to the casual user.

The first code block once agains sets up a few tracking variables for the eventual looping.

Creating a Python Function to Update Balances for All Months

Below, I take the successful looping code from above, strip out the comments and turn it into a Python function using the def statement. The only two inputs required to get the results we have achieved so far are:

The original loanInformation DataFrame from the excel spreadsheet in its original form (no sorting required)

The maxPayment, or the most the debtor can afford to pay each month including the minimum payments required by the lenders.

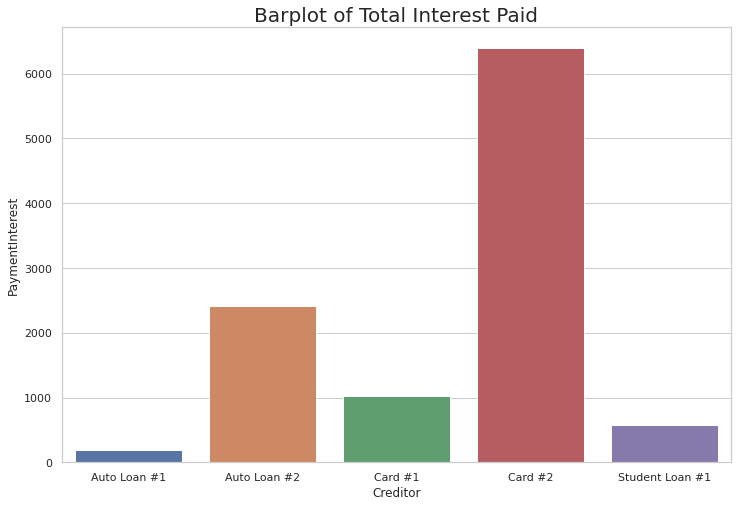

Plotting the Debt Snowball: Bar Chart of Interest Paid

Now that we have successfully calculated our results it is time to do something with them.

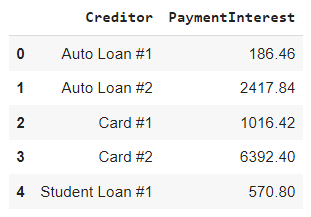

The first thing that might be interesting would be to visualize the amount of interest paid for each loan over the course repayment using the Snowball Method. To do this some data manipulation will need to occur. We will need to group all our results by Creditor and sum the interest components.

From there we will need to import 2 libraries to help us actually render the plot: matplotlib and seaborn. Both libraries are very well known and will help us present our data quickly. Below is the code and the Plot.

As you can see above, the prime offender when it comes to interest is Card #2. This is not the loan we attempted to pay off first with the snowball method.

In fact, Card #2 had the highest interest rate and largest balance… so we paid it off last. This clearly results in a situation where the debtor has paid off more interest than necessary. This highlights once again that when using the snowball, you are taking advantage of the psychological benefits of debt repayment and not necessarily mathematics.

Plotting the Debt Snowball: Timeline of Payoff

The following plot is an excellent way to visualize exactly how the snowball method functions. By plotting a line plot of each loan’s balance we will be able to see how the rate of change of repayment occurs.

The first loan paid off is Auto Loan #1 since it started with the smallest balance. Its rate of descent remains constant since it gets to use the snowball along with the minimum payment the entire time.

Moving to the left, the orange line shows how Card #1 declines over time. It descends only slightly until the first loan is paid off since its minimum payment barely covers any principal. Once the first loan is paid off it can use the snowball and the amount originally allocated to the monthly payment of Auto Loan #1. Once this occurs the balance drops much faster.

The same can be seen for each loan thereafter. As each loan is successively paid off, the next loan decreases in dramatic fashion.

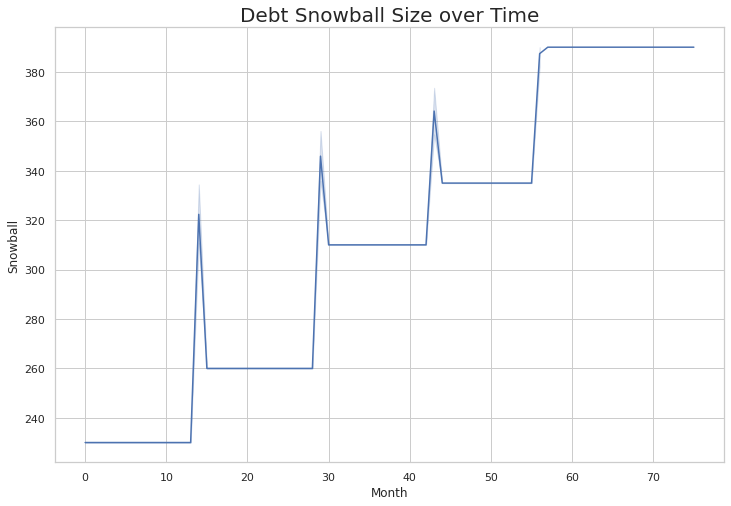

Plotting the Debt Snowball: Total Debt Over Time

The last chart I will show is not one that is necessarily interesting to someone who is repaying their debts. Rather, it shows that our function is working even when considering the nuances.

Consider that during a month that any of the loans are paid of there may be additional money available above and beyond what is owed for the last payment. The chart below shows that we are able to take care of this additional, albeit very small amount, correctly.

Notice the spike in debt snowball size during each of the months that a loan is fully paid off.