How to Use Python to Model Paying Off Your Mortgage Early

Purchasing a home is one of the biggest decisions an individual can make over the course of their entire lifetimes. Developing the credit history and income to convince a bank to fork over multiple times your annual salary is quite the feat. However, paying off your mortgage can often be just as big a of a decision.

Purchasing a home is one of the biggest decisions an individual can make over the course of their entire lifetimes. Developing the credit history and income to convince a bank to fork over multiple times your annual salary is quite the feat. However, paying off your mortgage can often be just as big a of a decision.

In this article I will show you how to wield Python to calculate the benefit of paying additional money towards your mortgage. Scenarios where an additional amount is paid every month, or even midway through the loan period will be considered.

Finally, I will show you how to plot this information out using the MatPlotLib and Seaborn libraries.

Graphically depicting the benefit of paying additional money towards your home loan can be quite motivational and a helpful explanatory tool when describing these benefits to others such as your spouse or even perhaps clients.

Amortizing the Mortgage

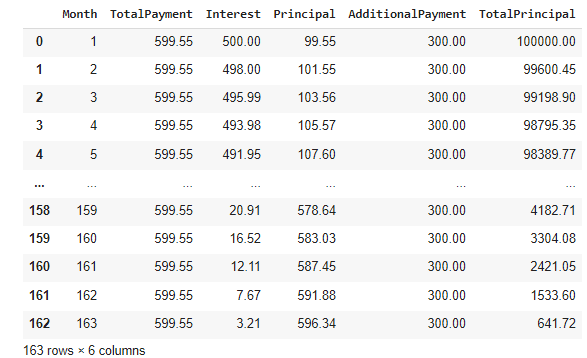

In another article I wrote, I showed how to use Python to Calculate Mortgage Amortization. The formula is fairly straightforward. To calculate the Total Monthly Payment for a Mortgage given the parameters set above you would use this formula:

Note: This formula should be used with the monthly interest rate for r. Our parameters set above use the more traditional annual interest rate. I will convert r to rM below which will account for this.

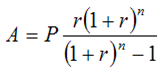

Finding the Payment Breakdown for All Months

Calculating the 1st month’s breakdown was simple. However, we now need to find the breakdown of interest and principal for each month of the entire loan.

Using a for loop I will populate a DataFrame called data. data will be initialized with the first month’s data at the outset. The principal paid in the first month will be subtracted from the overall principal remaining on the loan so that the next month’s interest can be calculated.

From there the process repeats until all months have been addressed and the final payment covers the entire remaining principal and accrued interest.

Taking a peek below at data reveals that there is a row for each month. The index runs from 0 to 359 and the final payment (row 359) is composed of the exact amount necessary to complete the terms of the mortgage.

Paying Additional: Calculating the Data

Now that we know how the original loan is amortized and how to calculate the breakdown of the interest and principal components for each payment it is time to add in our additional monthly payment.

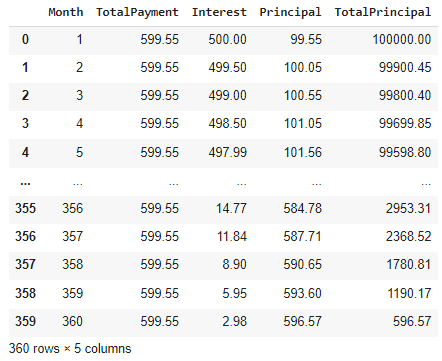

Below, the variable AdditionalPayment can be changed to account for whatever amount you would like to pay extra. I have set AdditionalPayment to $300. For this portion, the additional amount will be applied for all payments of the loan… even the first payment (we will cover more complicated scenarios later).

The setup for this calculation is almost exactly the same as for the original amortization. The resulting DataFrame will be called data_addpay.

The output of data_addpay can be seen below.

Notice that the number of Months in the final row is still 360. But does this make sense? It looks like the calculation just continued even after the loan was paid.

There are 2 main ways to tackle this:

- We could add an if statement into the for loop to escape earlier based on the value of

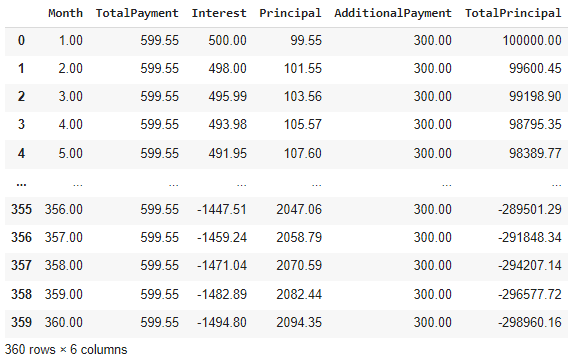

- We can just truncate the data that we have already calculated.

I will opt for the latter as seen below. The first step is to find PayOffMonths, or the number of months that will be used to truncate the data.

And the new version of data_addpay can be seen below to have only 163 rows as expected. We now have all the data necessary to make a quantitative comparison… and even make a plot!

Paying Additional: Plotting a Comparison to the Original Mortgage

With the data of both the original amortization and of the scenario where an additional payment of $300 is added on top of each month’s payment we can quickly plot how they compare.

We should expect two sloping lines. The original loan data will slope towards 0 after 360 months. The additional payment data should slope much more steeply and terminate at month 163.

As seen above, the plot appears as expected. We can clearly see the effect of paying additional. But what if we only start paying an additional amount starting at some point after month 1? This is likely the most useful consideration. We’ll cover this tweak in the next section.

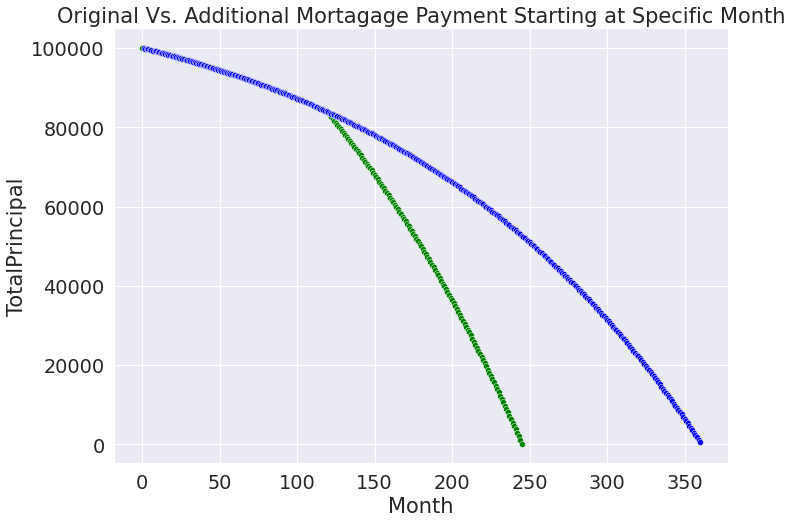

Paying Additional: Custom Start Date for Additional Payments

As a mortgage borrower, likely the decision to pay additional towards the principal will come at least a few months after you have started making payments. Perhaps it will be years. Whatever the case, it is easy to modify the code we have already wrote to account for this.

The initial data needed is below. The variable MonthStartContributing will be number of the montsh into the original loan period that the borrower intends to start adding an additional payment to be paid towards the principal.

The plot matches our original expectations.

Paying Additional: Plotting a Comparison to the Original Mortgage Part 3

Now let’s plot all 3 together. The code in this case is very much just a copy and paste of the above.

With this final plot is easy to confirm all our theories with the data that was calculated. Additionally, the code we have created is in perfect form to create our own function in Python which I will do in another article.

More complicated analytical investigations can be completed that vary both the additional payment used, interest rate, and other technical aspects of the mortgage with this work used as a basis.

Summary

In this article I have showed you how to calculate the amortization of your mortgage, apply an additional payment throughout the loan, and apply an additional payment partially through the loan. I have shown you how to plot the resulting data and think about how to evaluate the results to ensure their validity.

I hope you enjoyed this article! I will be adding more complicated scenarios as a follow-up and will post them here at DataDrivenMoney.com as always. Please feel free to throw positive or constructive comments in the section down below!