How to Use Python to Calculate Mortgage Amortization

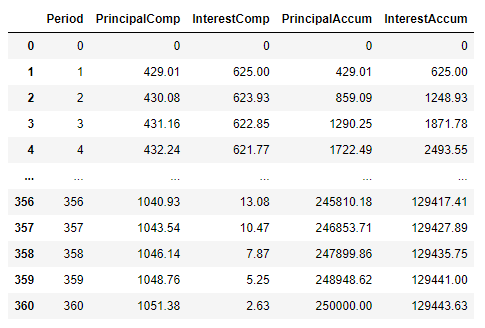

As we can see above, we now have a nice and tidy 361 row mat

rix of all of our interest and principal payments. We can easily export this data to excel using the following command:

payments.to_exce

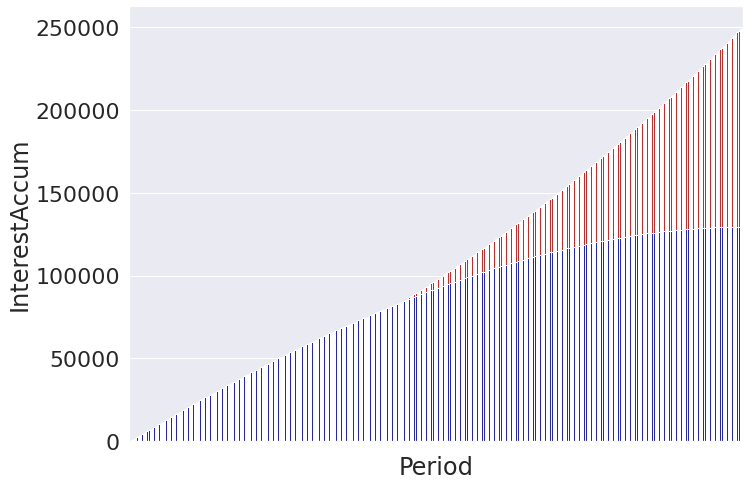

Obviously, if our initial loan was for $250,000 then our final total amount of principal paid should be the same amount… we can confirm this is true above. The total amount of interest paid, a more exciting number, is $129,443.63 for a 3% loan amortized over 30 years. Not so bad. We have all the data we need to plot out our payments and interest.l(‘payments.xls’) The last row of the DataFrame also tells us the cumulative interest and principal paid.

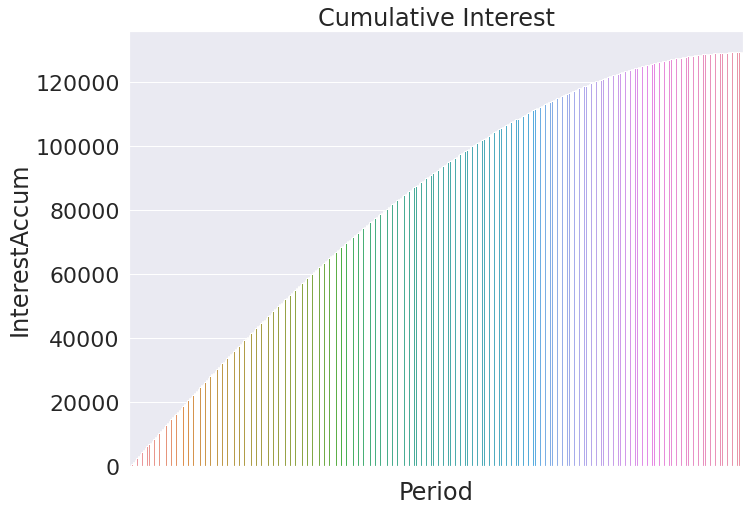

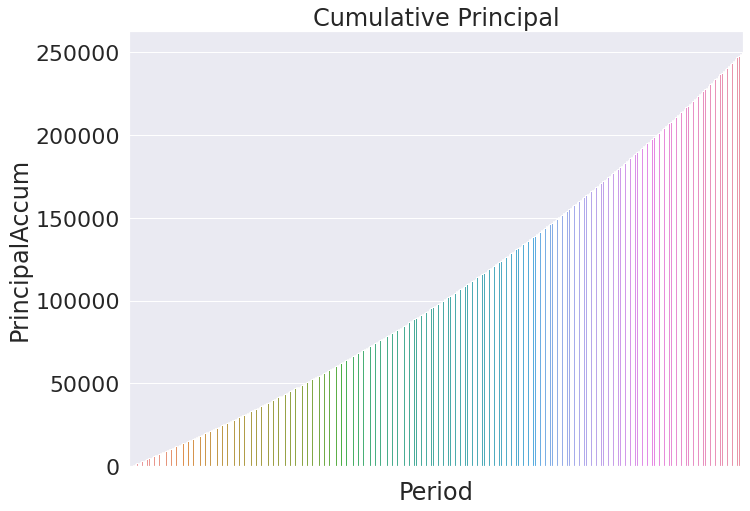

Now lets plot both on top of each other using the same type of bar chart.

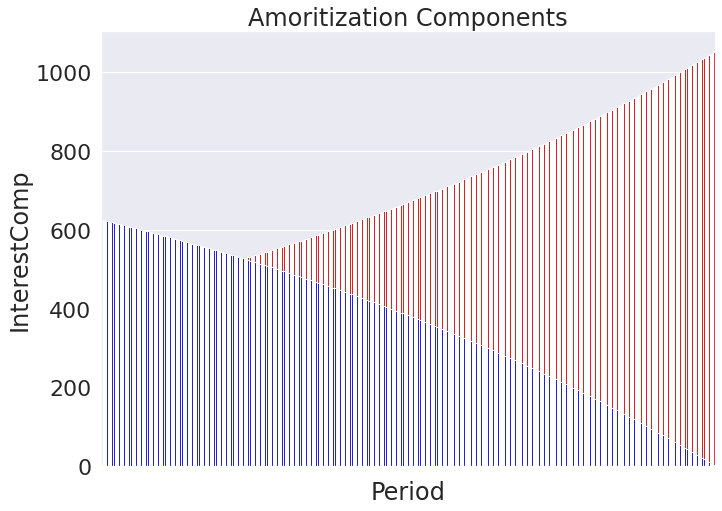

Now let’s see how the composition of the individual payments change over time. In theory the payment should skew more and more towards the principal since we have a smaller balance to pay interest and the monthly payment remains unchanged. The below chart should show the blue component going towards 0 while the principal peaks near the full monthly payment amount.

To make things easier lets see if we can use some type of line. Since we have many points that we can plot we can just use a scatter plot. The 360 rows of values should make the plot appear line like. Notice the blue dot at the bottom left that marks where we initialized our DataFrame to make our for loop work. By plotting it this way it is easier to see how the payment values change even when their values overlap.

Other Considerations:

So far in this article we have been able to calculate the monthly payment for a mortgage given the interest rate, principal, and time constraints. We then were able to graphicly discern how the payment is comprised of changing values for both the interest and principal despite the monthly payment remaining static. But there are other major considerations when discussing the amortization of a mortgage that should not be left out of the discussion.

PMI – Private Mortgage Insurance

Private mortgage insurance is a policy that you may have to pay on top of your principal and interest payment if you have a conventional loan. Typicall,y you only have to pay this if you did not put down at least 20% in cash as a down payment. If you have a VA loan, then this does not apply. Don’t forget to add this to your monthly amount if it applies to you.

Property Taxes

Property taxes can be a big deal depending on where you live. What state and whether you live inside city limits can change the amount you pay monthly quite dramatically. That said, you should talk to your mortgage broker or accountant to get a better idea how much this is so you can factor it into your calculations. Property taxes can often be larger than the interest you pay on your mortgage and can vary so much that a few miles difference can make the difference on whether you can afford a specific home or not so watch out.

Escrow

Many additional loan contingencies may require you to pay into an escrow. Sometimes the escrow account is the party that will be paying your property taxes or other fees mentioned already. Either way, you will need to get at least an estimate of what these fees will be and what your bank will require you to pay through your escrow. Only your bank can do this since they set the requirements. Usually, you will be paying into your escrow at the same time you are making your normal house payments.

HOA and COA Fees

Homeowners’ Associations (HOAs) or Condo Owners’ Associations (COAs) also usually levy a fee. Sometimes it is paid annually, semi-annually or for more expensive operations monthly. Don’t be caught off guard. For condos especially, HOA/COA fees can run into the 1,000s of dollars a month depending on the specific dynamics of the property you are looking at.

Home Maintenance

Maintenance is also something that needs to budgeted for. Although you will not likely need to pay anyone a set fee, it is a good idea to set aside some money each month into a low-risk account such as a savings account in the case you have an emergency repair. The contract language in your mortgage agreement likely requires you to make major repairs in a timely manner… saving ahead of time will help ensure that you keep on top of an unexpected outflows to your budget.

Maintenance is also something that needs to budgeted for. Although you will not likely need to pay anyone a set fee, it is a good idea to set aside some money each month into a low-risk account such as a savings account in the case you have an emergency repair. The contract language in your mortgage agreement likely requires you to make major repairs in a timely manner… saving ahead of time will help ensure that you keep on top of an unexpected outflows to your budget.

Conclusion and Financial Warning

Calculating your mortgage amortization is a great way to understand what underpins what is likely the largest purchase you will ever make. Additionally, it allows you to build the code necessary to start modeling out other parameters such as making additional lump sum payments each month. We’ll cover the additional things you can do with Python as it pertains to your mortgage in our next article. We’ll link it here once its complete.

All that said, understand that I have written this article as an expression of my opinion only. Please do your own research. Hire a qualified Financial Advisor, Mortgage Broker, or Accountant to give you specific advice tailored to your exact situation. Upon publishing this article, I am not aware of any coding mistakes… but I do make them… and I make them a lot. Please use the code at your own risk and reach out to me if you have any ideas down in the comments section or by email.